FII Exodus Meets DII Resilience: How India’s Institutional Investors Are Reshaping Market Dynamics in 2026

In the first quarter of 2026, a quiet revolution is reshaping the foundations of Indian capital markets. For the first time in India’s market history, the structural dominance of Foreign Institutional Investors (FIIs) is being convincingly challenged—and in many sessions outright neutralised—by the growing might of Domestic Institutional Investors (DIIs). This shift, years in the making, is now manifesting in ways that are fundamentally altering market dynamics, volatility patterns, and the very character of Indian equity investing.

The Numbers Tell a Compelling Story

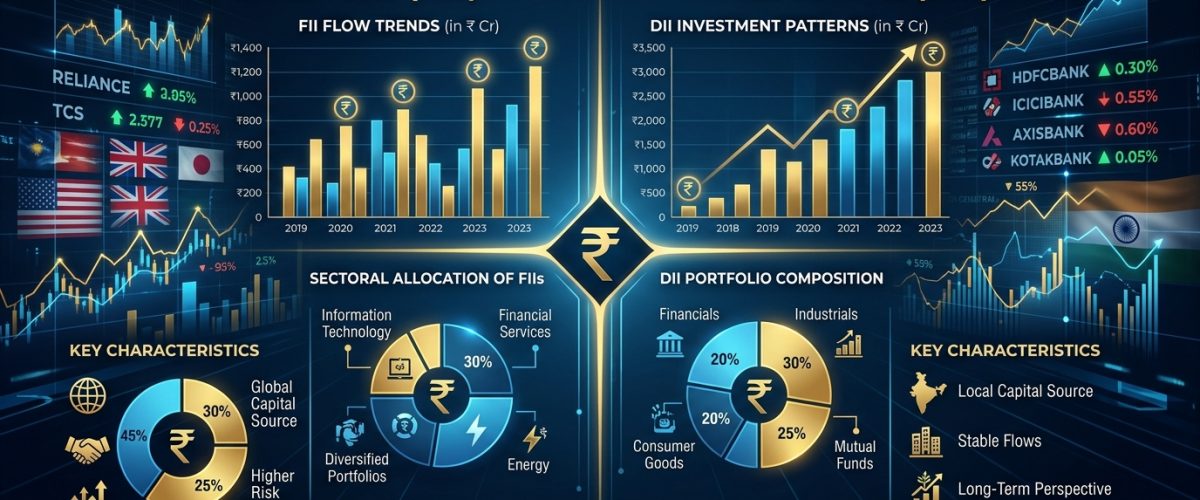

Foreign Portfolio Investors (FPIs) have been persistent net sellers in Indian equities during the first three months of 2026, with cumulative outflows exceeding ₹72,000 crore through mid-March. The selling has been driven by a confluence of global factors: elevated US Treasury yields making dollar-denominated assets more attractive, a stronger greenback, geopolitical uncertainties from the Israel-Iran conflict, and portfolio rebalancing away from emerging markets toward perceived safe havens.

In previous cycles, such sustained FII selling would have triggered sharp corrections in Indian markets. The Sensex crash of 2008, the taper tantrum of 2013, and the COVID-induced sell-off of 2020 all demonstrated how FII withdrawals could decimate Indian equity valuations. However, 2026 is writing a different script.

DIIs have purchased a net ₹85,000 crore worth of Indian equities in the same period, not merely absorbing FII selling but creating net positive institutional demand. This has kept the Nifty 50 within a relatively narrow trading range of 22,500-23,500, defying global volatility patterns that have seen other emerging market indices decline 8-15 per cent in the same period.

The SIP Juggernaut: India’s Structural Market Advantage

At the heart of DII strength is the Systematic Investment Plan phenomenon. Monthly SIP inflows into Indian mutual funds have consistently exceeded ₹23,000 crore in FY2025-26, with February 2026 recording an all-time high of ₹24,800 crore. The total number of SIP accounts has crossed 10 crore, representing roughly 7 per cent of India’s population—a figure that, while impressive, suggests enormous room for further penetration.

This structural flow creates a fundamentally different market dynamic from the one that prevailed a decade ago. “SIPs are the financial equivalent of a flywheel,” explained Nilesh Shah, Managing Director of Kotak Mahindra Asset Management. “Once the momentum builds, it becomes self-reinforcing. Investors who see their portfolios recover from dips thanks to rupee-cost averaging become more committed to the process, creating a virtuous cycle of participation.”

The monthly SIP book essentially provides Indian markets with a predictable demand floor of over ₹275,000 crore annually, making it increasingly difficult for any single category of sellers—including FIIs—to destabilise markets in a sustained manner.

Insurance and Pension Funds: The Silent Giants

Beyond mutual funds, India’s insurance companies and pension funds have emerged as significant equity market participants. The Life Insurance Corporation of India (LIC), the National Pension System (NPS), and the Employees’ Provident Fund Organisation (EPFO) collectively manage assets exceeding ₹65 lakh crore, with equity allocations gradually increasing in line with regulatory permissions and investment mandate modifications.

The NPS, in particular, has seen explosive growth. Total NPS assets under management crossed ₹14 lakh crore in early 2026, with the government’s decision to enhance the employer contribution limit under the new tax regime boosting enrolments. The NPS’s equity allocation, managed by professional fund managers across multiple schemes, provides a steady stream of long-term capital into Indian markets. These developments in personal investment echo the broader financial transformation India is witnessing, much like the growing commercial scale of IPL 2026 franchise strategies reflects the maturity of India’s sports business ecosystem.

What FII Selling Really Means in 2026

It would be premature to dismiss FII flows as irrelevant. Foreign investors still hold approximately 17 per cent of the free-float market capitalisation of NSE-listed companies, making them a significant constituency. More importantly, FII participation brings global best practices in corporate governance, analyst coverage, and market microstructure that benefit the ecosystem as a whole.

However, the nature of FII participation is evolving. Long-term foreign investors—sovereign wealth funds, large pension funds, and dedicated emerging market mandates—have largely maintained their Indian allocations. The selling has been concentrated among hedge funds, momentum-driven strategies, and global macro funds that use Indian markets as a proxy for broader emerging market sentiment.

This bifurcation suggests that while tactical FII flows will continue to create short-term volatility, the strategic allocation to India remains intact. Discussions with several large global asset allocators confirm that India remains a consensus overweight in emerging market portfolios, with the current selling viewed as a temporary response to global rather than India-specific factors.

Implications for Retail Investors and Market Structure

The DII-led market has several practical implications for Indian retail investors. First, the reduced dependence on FII flows means that Indian markets are becoming less correlated with global risk-on/risk-off cycles, potentially improving their diversification value in global portfolios. Second, the steady DII bid at lower levels has compressed downside volatility, making deep corrections less likely but also potentially limiting the magnitude of sharp rallies.

Third, and perhaps most significantly, the growing domestic institutional ownership is shifting the market’s centre of gravity. Stocks and sectors favoured by domestic funds—banking, consumption, infrastructure, and select manufacturing plays—are likely to outperform over the medium term, while globally linked sectors such as IT and metals may see more muted institutional support unless global conditions improve.

Market structure itself is evolving. The NSE and BSE have seen a significant increase in retail participation through direct equity investing as well, with demat account numbers crossing 18 crore. The combination of direct retail investing and indirect participation through SIPs has created what some analysts describe as a “domestic ownership renaissance” in Indian capital markets.

The Road Ahead: Sustainability of DII Dominance

The critical question for market observers is whether DII dominance is sustainable. Several factors suggest it is. India’s demographic profile—with a median age of 28 and a rapidly growing working-age population—ensures that the pool of potential investors will continue to expand. Financial literacy initiatives by SEBI, AMFI, and the broader mutual fund industry are gradually reaching smaller cities and towns, expanding the addressable market.

Moreover, the regulatory environment is supportive. SEBI’s measures to improve market transparency, protect retail investors, and encourage long-term investing have created a more trustworthy ecosystem. As discussed in our analysis of how India’s tech ambitions reveal structural challenges, regulatory frameworks that balance growth with protection are critical to sustainable development across sectors.

The FII-DII dynamic of 2026 may well be remembered as the year Indian markets truly came of age—the year when domestic capital conclusively demonstrated its ability to anchor the world’s fifth-largest equity market, regardless of the direction of global capital flows.

- Startup India at 10: A Decade of Disruption and the Founders Who Shaped the Ecosystem - March 24, 2026

- From Side Hustles to Success: Five Indian Founders Who Turned Adversity Into Billion-Dollar Ventures - March 24, 2026

- Healthtech Funding Shifts Toward Integrated Care Models as Investors Eye Sustainable Growth in India - March 24, 2026