Indian Stock Markets Navigate Geopolitical Turbulence as Nifty Holds Above 23,100 in March 2026

Indian equity markets demonstrated remarkable resilience in the third week of March 2026, with the benchmark Nifty 50 index closing above the psychologically significant 23,100 mark despite persistent geopolitical headwinds stemming from the Israel-Iran conflict and volatile global crude oil prices. The 30-share BSE Sensex advanced 325.72 points, or 0.44 per cent, to settle at 74,532.96, while the Nifty 50 rose 112.35 points to close at 23,114.50 on Friday, March 20.

A Session Defined by Volatility and Selective Buying

Friday’s trading session epitomised the broader narrative of Indian markets in March 2026—extreme intraday swings tempered by strong institutional support at lower levels. The Sensex surged as much as 1,079 points during the day to touch an intraday high of 75,286.39, only to surrender a large portion of those gains by the close. Similarly, the Nifty touched 23,345.15 before retreating.

Market analysts attributed the volatility to a tug-of-war between optimism over domestic fundamentals and anxiety about escalating tensions in West Asia. Crude oil prices, which had spiked above $90 per barrel earlier in the week on fears of supply disruptions, remained a critical variable for India, the world’s third-largest oil importer.

“The market is essentially pricing in two competing narratives,” said Deepak Jasani, Head of Retail Research at HDFC Securities. “On one hand, India’s macro story remains compelling—strong GDP growth, moderating inflation, and supportive monetary policy. On the other, geopolitical risk premiums are keeping a lid on any sustained rally.”

Sectoral Winners: PSU Banks, IT, and Metals Lead the Charge

Among the Sensex constituents, the rally was led by a diverse set of stocks. Tata Steel surged on the back of improved global metal prices and strong domestic demand for steel in infrastructure projects. Technology majors Tech Mahindra and Infosys gained as the rupee’s relative stability against the dollar and continued deal momentum in the IT sector boosted sentiment.

PSU banking stocks emerged as a notable outperformer during the week, with the Nifty PSU Bank index gaining over 3 per cent. Analysts pointed to improving asset quality, robust credit growth of 14.5 per cent year-on-year as of February 2026, and the government’s continued push for financial inclusion as key tailwinds. State Bank of India, Bank of Baroda, and Canara Bank all posted solid weekly gains.

The energy sector also attracted attention, with Reliance Industries rising as the company’s diversified revenue streams—from petrochemicals to digital services and retail—provided a natural hedge against crude oil volatility. NTPC gained on expectations that India’s power demand would continue its upward trajectory, driven by data centre expansion and industrial growth.

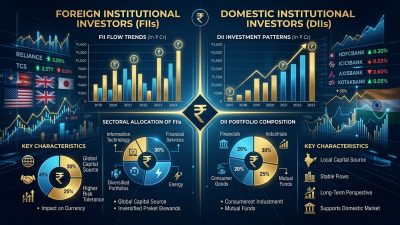

FII vs DII: The Institutional Battle Intensifies

A defining feature of Indian markets in early 2026 has been the contrasting behaviour of Foreign Institutional Investors (FIIs) and Domestic Institutional Investors (DIIs). Foreign portfolio investors have been net sellers for much of the quarter, pulling out approximately ₹28,000 crore from Indian equities in March alone, driven by a stronger US dollar, higher US Treasury yields, and geopolitical risk aversion.

However, DIIs—comprising mutual funds, insurance companies, and pension funds—have more than offset FII outflows. DII net purchases in March exceeded ₹35,000 crore, reflecting the sustained flow of domestic savings into equity markets through Systematic Investment Plans (SIPs). Monthly SIP contributions have consistently remained above ₹23,000 crore, providing a structural floor for Indian equities.

This dynamic has fundamentally altered the character of Indian markets. Where once FII flows dictated direction, domestic institutional participation now provides a significant counterbalance, reducing the impact of foreign capital flight on benchmark indices. As explored in our coverage of India’s AI Summit 2026 and its structural challenges, the country’s growing technological and institutional maturity is increasingly reflected in its financial markets as well.

Macro Backdrop: Why India’s Growth Story Remains Intact

The Reserve Bank of India’s decision to hold the repo rate at 5.25 per cent in February 2026—following a 25 basis point cut in December 2025—has provided markets with a stable monetary policy environment. With inflation at 1.33 per cent in December 2025, well below the RBI’s 2-6 per cent tolerance band, there is growing expectation that the central bank could deliver another rate cut at its April meeting.

India’s GDP growth forecast for FY2025-26 stands at 7.4 per cent, revised upward from 7.3 per cent, with the economy benefiting from increased government capital expenditure, robust private consumption, and the positive spillover effects of US-India trade agreements signed earlier in the fiscal year.

Small and Mid-Cap Segments: Caution Amid Opportunity

While large-cap indices have shown measured gains, the broader market has exhibited greater stress. The Nifty Smallcap 100 index has corrected over 12 per cent from its February highs, as stretched valuations and profit-booking by retail investors weighed on sentiment. Market regulators at SEBI have also issued advisory notes to mutual fund houses about managing small-cap fund inflows and maintaining adequate liquidity buffers.

Fund managers suggest that the correction in small and mid-caps, while painful, is ultimately healthy. “Valuations in certain pockets of the small-cap universe had become disconnected from fundamentals,” noted Rajeev Thakkar, CIO of PPFAS Mutual Fund. “This correction creates opportunities for long-term investors to build positions in quality names at more reasonable valuations.”

Looking Ahead: Key Catalysts for April and Beyond

As March draws to a close, market participants are focused on several upcoming catalysts. The RBI’s monetary policy announcement on April 8 will be closely watched for signals on further rate cuts. The onset of Q4 FY26 corporate earnings season in mid-April will provide crucial data on whether India Inc’s profitability is keeping pace with topline growth.

The geopolitical situation in West Asia remains the primary wildcard. Any de-escalation could trigger a sharp relief rally, while further escalation—particularly any disruption to oil supplies through the Strait of Hormuz—could push crude prices higher and weigh on Indian markets through imported inflation and a widening current account deficit.

For now, the consensus view remains cautiously optimistic. India’s domestic fundamentals, institutional investment flows, and structural reform momentum continue to make it one of the more attractive emerging market destinations, even as global uncertainties demand a measured approach to portfolio allocation.

- Startup India at 10: A Decade of Disruption and the Founders Who Shaped the Ecosystem - March 24, 2026

- From Side Hustles to Success: Five Indian Founders Who Turned Adversity Into Billion-Dollar Ventures - March 24, 2026

- Healthtech Funding Shifts Toward Integrated Care Models as Investors Eye Sustainable Growth in India - March 24, 2026