India Drops to 7th Largest Stock Market as South Korea and Taiwan Overtake on AI Semiconductor Boom

In the span of just over a week, India’s stock market has gone from being the world’s fifth-largest to the seventh-largest by market capitalisation — overtaken first by Taiwan and then by South Korea as artificial intelligence-driven semiconductor rallies propel both Asian markets to record highs.

The Numbers Tell a Stark Story

South Korea’s stock market capitalisation surged to $5 trillion after an extraordinary 86 percent rally in 2026, driven almost entirely by Samsung Electronics and SK Hynix — the world’s two largest memory chip manufacturers. India’s market cap, meanwhile, has slipped to approximately $4.8 trillion, creating a gap of $200 billion that did not exist two weeks ago.

Taiwan’s overtaking came first, powered by Taiwan Semiconductor Manufacturing Company (TSMC), which has seen a record 50 percent rally this year and now accounts for over 40 percent of the entire Taiwan Stock Exchange’s market capitalisation. In South Korea, Samsung and SK Hynix together represent a similarly outsized share of the KOSPI index’s gains.

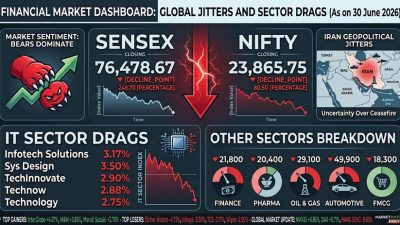

The shift is remarkable given India’s trajectory. The BSE Sensex hit a lifetime intra-day high of 86,159 on 1 December 2025, when India held the fifth spot globally behind only the United States, China, Japan, and the United Kingdom. Since that peak, Indian markets have fallen over 13 percent — a double-digit decline that has been accelerated by the US-Iran conflict since March 2026.

What Is Driving the Semiconductor Markets

The divergence between India and its Asian peers is almost entirely explained by one factor: the global AI infrastructure buildout. The world’s largest technology companies — led by Nvidia, Microsoft, Google, Meta, and Amazon — are spending hundreds of billions of dollars building data centres to train and run artificial intelligence models. This spending requires vast quantities of advanced semiconductors, and the supply chain for these chips runs through Taiwan and South Korea.

TSMC manufactures the most advanced chips in the world, including Nvidia’s AI processors. SK Hynix produces the High Bandwidth Memory (HBM) chips that are essential for AI workloads. Samsung, while also a memory chip leader, benefits from the same demand cycle. Nvidia itself has become the world’s most valuable company, with a market cap exceeding $5 trillion and a one-year stock price rally of over 63 percent.

India’s stock market, by contrast, has no equivalent beneficiary of the AI boom. The country’s technology sector is dominated by IT services companies — Tata Consultancy Services, Infosys, Wipro — whose business model of labour-cost arbitrage does not capture the value created by AI hardware demand. India’s nascent semiconductor manufacturing ambitions are years away from producing companies of global scale.

Foreign Investors Have Been Leaving

The market cap decline is not just a relative phenomenon. Foreign portfolio investors (FPIs) have been net sellers of Indian equities for most of 2026, withdrawing over Rs 1.5 lakh crore (approximately $17 billion) from Indian markets as global capital flows toward AI-linked assets in the US, Taiwan, and South Korea.

Domestic institutional investors and retail traders have partially offset the selling, but not enough to prevent the Sensex from entering a sustained downtrend. The Nifty 50 index, which tracks India’s largest companies, is trading more than 15 percent below its all-time high, with banking, real estate, and consumer discretionary sectors bearing the brunt of the correction.

The US-Iran war has compounded the problem. Elevated crude oil prices — Brent has traded between $90 and $110 per barrel for most of 2026 — directly pressure India’s current account deficit, inflation expectations, and corporate margins. The uncertainty has made global fund managers reluctant to increase India allocations at a time when semiconductor stocks offer clearer near-term returns.

Is This a Temporary Blip or a Structural Shift

Optimists argue that India’s drop to seventh is a cyclical phenomenon that will reverse once the AI hardware cycle matures and geopolitical conditions stabilize. India’s long-term growth story — demographic dividend, digitisation, expanding domestic consumption — remains intact. The country’s GDP growth rate of 6.5 percent remains among the fastest of any major economy.

However, sceptics point to structural weaknesses. India’s market valuation at its peak was partly supported by speculative retail flows into small-cap and mid-cap stocks — a segment that has corrected sharply. The country’s technology sector needs a fundamental upgrade from services to products and semiconductors to participate in the current global rally. That transition will take a decade, not a quarter.

“India’s stock market was priced for perfection at 86,000 Sensex,” noted a senior fund manager at a Mumbai-based asset management firm. “What we’re seeing now is a repricing to reality. The AI-driven rally in East Asia is genuine economic value creation — TSMC and Samsung are building real things the world needs. India needs to find its equivalent.”

What India Can Learn

The lesson from Taiwan and South Korea is that concentrated bets on strategic industries can deliver outsized returns. TSMC was built through decades of government-backed industrial policy, subsidized R&D, and a single-minded focus on becoming indispensable to the global chip supply chain. South Korea’s chaebols invested aggressively in memory chip capacity during downturns, positioning Samsung and SK Hynix to dominate when demand returned.

India’s $10 billion semiconductor incentive programme, announced in 2021, has attracted interest from Tata Electronics, the Vedanta-Foxconn joint venture, and Israel’s Tower Semiconductor. But none of these facilities will produce chips at the cutting-edge nodes that drive AI valuations. For India to climb back up the global market rankings, it needs both time and a willingness to accept that some industrial investments may take a generation to pay off.

In the near term, Indian investors should brace for volatility. The AI rally shows no signs of peaking, the geopolitical environment remains uncertain, and the structural gap between India’s economy and its stock market valuations is being ruthlessly repriced by global capital.