Venture Capital Returns to India: Inside the Funding Rebound and What’s Changed for Startups

The Funding Winter Thaws as Investor Confidence Rebuilds

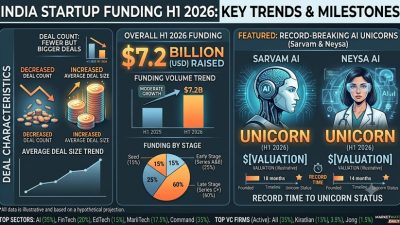

After nearly two years of cautious capital deployment that industry participants dubbed the “funding winter,” venture capital investment in Indian startups is staging a decisive comeback in 2026. The recovery is unmistakable: Q1 2026 saw 315 funding rounds worth approximately $3.5 billion, representing a 40 per cent increase in volume and a 55 per cent increase in value compared to Q1 2025. More importantly, the quality of deals has improved significantly, with investors backing companies that have demonstrated the ability to grow efficiently rather than merely rapidly.

The thaw began in the second half of 2025, when several prominent exits—including successful IPOs by FirstCry (Brainbees Solutions), Ola Electric, and Go Digit Insurance—demonstrated that the Indian startup ecosystem could generate meaningful returns for investors. These liquidity events, combined with improving macroeconomic conditions and a stabilising global interest rate environment, restored the risk appetite that had been severely dampened by the correction of 2022-2024.

How Investor Behaviour Has Fundamentally Changed

The most consequential development in India’s venture capital landscape is not the quantum of capital being deployed but the philosophy governing its deployment. The investment thesis that dominated the 2019-2021 period—characterised by aggressive growth financing, winner-take-all market share battles, and tolerance for negative unit economics—has been decisively replaced by a framework that prizes sustainable business building.

This shift manifests in several observable ways. Due diligence processes have lengthened from 2-4 weeks to 8-12 weeks, with investors conducting deeper analysis of unit economics, customer acquisition cost trends, and retention metrics. Valuation multiples have compressed to more sustainable levels, with revenue multiples of 8-15x for SaaS companies and 3-5x for consumer businesses, compared to 30-50x multiples seen during the bubble. Board-level governance expectations have also intensified, with investors increasingly insisting on independent directors, audit committees, and transparent financial reporting from the earliest stages.

The composition of the investor base has also evolved. While global mega-funds like Tiger Global and SoftBank remain active, their approach is markedly more selective, with smaller cheque sizes and higher return thresholds. Domestic venture capital firms—Peak XV Partners, Accel, Blume Ventures, and Chiratae Ventures—have gained prominence, leveraging their on-ground presence and deeper understanding of Indian market dynamics to source and evaluate deals more effectively. A deeper look at India’s technology landscape, including the developments around AI Summit 2026 and India’s tech ambitions, reveals the kind of foundational trends that are guiding investment decisions.

The Rise of Profitability-First Startups

One of the most encouraging trends in India’s 2026 startup ecosystem is the emergence of a cohort of companies that have achieved profitability or clear profitability trajectories while maintaining strong growth rates. Zerodha, which has been profitable since inception, serves as the aspirational model, but a growing list of companies—including CRED, PhonePe, Razorpay, and Dream11—have either achieved profitability or are approaching break-even ahead of schedule.

This profitability-first cohort has been rewarded by the market. Zepto, the quick commerce startup, raised its latest round at a valuation premium to competitors partly because of its superior unit economics at the dark store level. Similarly, PhysicsWallah’s combination of rapid growth and profitability has attracted premium valuations in the edtech sector, a space where most competitors have struggled to reconcile growth with financial sustainability.

The cultural shift toward profitability is also visible in how startups communicate their achievements. Where press releases in 2021 focused exclusively on GMV (Gross Merchandise Value) and user growth, the 2026 narrative centres on EBITDA margins, contribution margins, and customer lifetime value. This linguistic shift reflects a deeper transformation in founder mindsets, driven by the harsh lessons of the funding winter and the recognition that sustainable businesses, not just large businesses, attract the best investors and the highest valuations.

Sectoral Investment Trends: Where Capital Is Flowing

The distribution of venture capital across sectors in Q1 2026 reveals clear investor preferences. Fintech continues to attract the largest share (approximately 25 per cent of total funding), but the focus has shifted from consumer-facing payment apps to enterprise fintech, lending infrastructure, and insurance technology. Companies building the backend infrastructure of India’s financial system—payment gateways, credit scoring engines, regulatory compliance tools—are receiving disproportionate investor attention.

Enterprise SaaS (Software as a Service) remains a high-conviction category, with Indian startups like Freshworks, Zoho, and Postman having established that world-class software products can be built from India for global markets. The newer cohort of SaaS companies focuses on vertical solutions—industry-specific software for healthcare, construction, logistics, and retail—where deep domain expertise creates competitive moats that are harder for horizontal platforms to replicate.

Consumer technology, which dominated funding during the boom years, has seen a relative decline in investor interest. The quick commerce segment is an exception, with Zepto, Blinkit, and Swiggy Instamart continuing to raise capital as they compete for market share in the rapidly growing instant delivery market. However, other consumer categories—social media, content platforms, and subscription services—face scepticism from investors who question the path to profitability in India’s price-sensitive consumer market.

The Evolving Exit Landscape

The viability of India’s startup ecosystem ultimately depends on its ability to generate liquidity for investors through exits—whether via IPOs, strategic acquisitions, or secondary sales. The exit landscape has improved meaningfully in 2025-2026, with over 15 startup IPOs completed and several large M&A transactions announced.

The public markets have been receptive to well-managed startup listings, though the performance has been bifurcated. Companies with clear profitability—like Mamaearth (Honasa Consumer) and Ixigo—have traded well post-listing, while those that went public with significant losses have faced investor scepticism and price declines. This bifurcation has reinforced the message that public market investors, unlike growth-stage VCs, have limited patience for loss-making business models.

Strategic acquisitions have also picked up, with the Unacademy-upGrad merger being the most notable recent example. Corporate acquirers—including Reliance, Tata, and the Adani Group—are increasingly viewing startup acquisitions as a route to acquiring technology capabilities and market access, adding another exit pathway for investors. The broader economic context, including the stock market rally in March 2026, has created a favourable environment for IPO activity.

What 2026 Means for the Indian Startup Story

The funding rebound of 2026 is not merely a cyclical recovery but represents the maturation of India’s startup ecosystem into a more sustainable and sophisticated market. The painful corrections of 2022-2024, while devastating for some companies and investors, have ultimately strengthened the ecosystem by weeding out unsustainable business models, instilling financial discipline, and realigning incentives between founders and investors.

India now has over 110 unicorns, a robust pipeline of pre-unicorn companies, an increasingly sophisticated investor base, and a supportive regulatory and policy framework. The startup ecosystem contributes directly to employment (over 15 lakh direct jobs), innovation (India ranks among the top five countries in patent filings), and economic dynamism. As venture capital returns to India with renewed conviction, the stage is set for a more sustainable chapter of the Indian startup story—one where value creation, not just valuation creation, defines success. This optimism extends across India’s vibrant landscape, from economic fundamentals to Bollywood’s creative renaissance in March 2026.