Indian Markets See Brief Rally Before Record FII Outflows in March 2026

Indian Markets Saw Brief Recovery in Mid-March 2026 Before Record FII Sell-Off

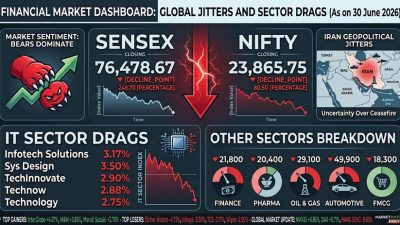

The Bombay Stock Exchange’s benchmark Sensex index briefly touched the 74,500 mark in mid-March 2026, raising hopes of a sustained recovery after months of volatility. However, the rally proved short-lived as foreign portfolio investors (FPIs) staged a historic exit from Indian equities, making March 2026 the worst month on record for foreign outflows.

By the end of March, the Sensex had fallen to approximately 71,947—a decline of over 10 per cent from its recent highs—as a confluence of geopolitical instability, rising energy costs, and a weakening rupee prompted global fund managers to retreat from riskier emerging market assets.

Record FII Outflows Dominate March 2026

The defining story of March 2026 was not a resumption of foreign buying but rather a record sell-off. Foreign portfolio investors withdrew approximately $12.3 billion (₹1.14 lakh crore) from Indian equities during the month—the largest single-month outflow ever recorded. This dwarfed the selling seen during previous episodes of foreign exodus and extended a broader trend: between October 2025 and March 2026, cumulative FII outflows from Indian equities exceeded ₹2.5 lakh crore.

Analysts attribute the sell-off to multiple factors: uncertainty around US trade policy and tariffs, rising US Treasury yields that made dollar-denominated assets more attractive, elevated crude oil prices due to US-Iran tensions, and concerns about the Indian rupee’s depreciation trajectory.

Domestic institutional investors (DIIs), including mutual funds, continued to provide support. Mutual fund SIP inflows remained above ₹25,000 crore monthly, offering a consistent demand base. However, DII buying was insufficient to offset the scale of foreign selling, resulting in broad market declines across large-cap, mid-cap, and small-cap segments.

Sectoral Impact: Banking Under Pressure, IT a Mixed Bag

The banking sector, which had initially led the mid-March bounce, gave back most gains as the sell-off intensified. HDFC Bank, ICICI Bank, and State Bank of India all saw significant volatility. The RBI’s February 2026 decision to hold the repo rate at 5.25 per cent provided some stability for the financial sector outlook, but concerns about asset quality in a slowing growth environment weighed on sentiment.

Information technology stocks presented a mixed picture. While the weakening rupee improved earnings visibility for IT exporters like TCS, Infosys, and HCLTech, broader concerns about global technology spending and the impact of AI-driven automation on traditional IT services created uncertainty, as highlighted in discussions around India’s AI Summit 2026 and its structural challenges.

Geopolitical Risks: Oil Prices and Trade Uncertainty

Rising tensions between the United States and Iran pushed Brent crude oil prices above $82 per barrel during March, a level that raises significant concerns for oil-importing nations like India. Every $10 increase in crude oil prices is estimated to widen India’s current account deficit by approximately 0.4 per cent of GDP, putting additional pressure on the rupee and import-dependent sectors.

Compounding the oil price risk, uncertainty around US trade policy—including the threat of broader tariffs—added to the risk-off sentiment in emerging markets. India, while relatively insulated compared to some export-dependent Asian economies, was not immune to the global reassessment of risk.

Retail Investor Participation Remains Strong

Despite the challenging market conditions, retail investor participation continued to grow. Data from the Central Depository Services Limited (CDSL) shows that total demat accounts in India crossed 18 crore in early 2026, with lakhs of new accounts opened each month. The sustained retail engagement, primarily through systematic investment plans, has fundamentally altered the character of Indian markets, making them more resilient to FII-driven swings than in previous cycles.

Young investors in the 25–35 age group continue to allocate income to equities through SIPs, representing a structural shift in Indian savings behaviour from fixed deposits and gold to financial assets.

Outlook: Caution Ahead of Q4 Results and April MPC Meeting

As April 2026 begins, market participants are watching two key events: the Q4 FY26 earnings season and the RBI’s Monetary Policy Committee meeting scheduled for April 6–8, 2026. Consensus estimates suggest that Nifty 50 companies may deliver earnings per share growth of 12–14 per cent for FY26, though the recent market turbulence has tempered expectations.

Goldman Sachs Research expects India’s real GDP to grow at 6.9 per cent in calendar year 2026, supported by domestic consumption, infrastructure investment, and an improving position in global supply chains. However, the firm has flagged trade policy uncertainty and elevated energy costs as key downside risks.

The Union Budget 2026-27’s emphasis on fiscal discipline—targeting a fiscal deficit of 4.4 per cent of GDP—and capital expenditure exceeding ₹11 lakh crore have been broadly well received. However, the near-term market direction will likely depend on whether FII selling abates and whether Q4 corporate earnings can justify current valuations.

Technical analysts note that the Nifty faces support around 22,000–22,600 levels, with a break below potentially triggering further correction. Investors are advised to maintain diversified portfolios and focus on companies with strong fundamentals rather than chasing short-term momentum.

Correction (3 April 2026): An earlier version of this article, published mid-March, framed a temporary market bounce as a sustained rally and cited ₹18,000 crore in FII inflows. In reality, March 2026 saw record FII outflows of approximately $12.3 billion (₹1.14 lakh crore), and the Sensex subsequently fell over 10% to approximately 71,947 by month-end. The article has been substantially revised to accurately reflect market conditions.