India Hikes Gold and Silver Import Duty From 6 to 15 Percent in Emergency Move to Protect Forex Reserves Amid Global Energy Crisis

The Indian government on Wednesday, 13 May 2026, announced a sharp increase in customs duties on gold and silver, raising the rate from 6 per cent to 15 per cent in a single emergency notification — the largest one-time duty hike on precious metals in over a decade. The move comes just two days after Prime Minister Narendra Modi publicly appealed to Indians to stop buying gold for at least a year, citing the strain that gold imports place on the country’s foreign exchange reserves amid the ongoing global energy crisis triggered by the Iran war and the prolonged disruption of the Strait of Hormuz.

The duty increase, effective immediately, also covers platinum (raised from 6.4 per cent to 15.4 per cent), as well as gold and silver doré, coins, findings, and related items. A Finance Ministry source told reporters that the move was “intended to moderate avoidable import demand and ease pressure on the external account,” adding that it was “neither prohibitory nor anti-consumer in nature” but a “prudent macroeconomic adjustment to extraordinary external conditions.”

Why the Government Acted Now

India’s foreign exchange reserves have fallen sharply in recent months as the country grapples with the consequences of the West Asia conflict that has sent crude oil prices above $100 per barrel and disrupted global trade routes. According to the latest Reserve Bank of India (RBI) data, forex reserves declined to approximately $690 billion in the week ended 1 May, down from an all-time high of $728.49 billion during the week ended 27 February — a fall of nearly $38 billion in just two months.

The decline has been driven by multiple factors: the RBI’s intervention to defend the rupee, which has weakened significantly against the dollar; higher oil import bills as Brent crude has traded above $95–105 per barrel since March; and continued outflows by foreign portfolio investors who have withdrawn over Rs 2 lakh crore from Indian equities in 2026. Against this backdrop, gold imports — which consume approximately $35–40 billion of forex annually — have been identified as a category where demand can be moderated without affecting economic growth or food security.

PM Modi’s Gold Boycott Appeal

The duty hike follows PM Modi’s highly publicised appeal on 11 May during a BJP rally in Hyderabad, where he urged citizens to adopt a series of austerity measures in response to the global crisis. Among these, the most striking was his call for Indians to avoid purchasing gold for at least one year. “Gold purchases are another area where foreign exchange is used extensively. In the national interest, we must resolve not to purchase gold for a year,” the Prime Minister said.

Modi’s appeal also included requests to reduce cooking oil consumption by 10 per cent, cut back on petrol and diesel use, delay international travel, and embrace austerity as a patriotic duty during the energy crisis. The gold import duty hike translates the Prime Minister’s appeal into concrete policy action, providing a fiscal disincentive for discretionary gold purchases while generating additional customs revenue for the government.

Impact on Gold Prices in India

The immediate impact of the duty hike was visible in domestic gold markets. The price of 10 grams of 24-carat gold surged past Rs 1,52,000 on Wednesday morning, incorporating the additional duty component. Industry analysts estimated that the 9 percentage point increase in duty translates to an additional Rs 12,000–14,000 per 10 grams at current international gold prices, which have been trading near all-time highs above $2,400 per ounce on the global market.

Silver prices also spiked, with MCX silver futures climbing over Rs 22,000 to touch an intraday high of Rs 3,01,429 per kilogram — crossing the psychologically significant Rs 3 lakh mark for the first time in Indian markets. Physical silver prices in major cities rose to approximately Rs 290 per gram, up from Rs 266 per gram the previous day.

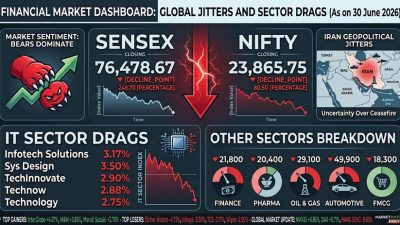

The gold and silver market rally has been fuelled by a combination of factors beyond the duty hike: global safe-haven demand driven by the Iran war, a weakening rupee (which makes dollar-denominated gold more expensive in India), and declining confidence in equity markets following the recent stock market rout that saw the Sensex crash over 3,000 points in four sessions.

The Jewellery Industry Reacts

The jewellery industry expressed shock at the magnitude of the duty increase. The All India Gem and Jewellery Domestic Council (GJC) said the hike would “significantly impact consumer sentiment and organised retail” while potentially boosting smuggling and the grey market for gold. Titan Company and Kalyan Jewellers — two of the largest listed jewellery retailers — saw their shares decline between 4 and 6 per cent in early trade on Wednesday.

The India Bullion and Jewellers Association (IBJA) warned that the sharp duty increase could lead to a surge in gold smuggling, which historically increases when the differential between international and domestic prices widens. The association noted that the previous duty hike to 15 per cent in 2013 had been followed by a significant increase in gold smuggling through airports and sea routes, and urged the government to strengthen enforcement alongside the fiscal measure.

Broader Macroeconomic Context

The duty hike must be understood in the context of India’s worsening current account dynamics. With crude oil imports consuming a much larger share of forex reserves due to elevated prices, the government is prioritising essential imports over discretionary ones. Sources indicated that the measure was designed to “prudently manage emerging risks and reduce vulnerability to potential external shocks before pressures on the current account intensify further.”

India imports roughly 700–800 tonnes of gold annually, making it the world’s second-largest consumer of the metal after China. Gold imports constitute the second-largest component of India’s import bill after crude oil, and any reduction in gold import volumes directly eases pressure on the current account deficit and the rupee.

The rising inflationary pressures in the economy — with CPI inflation climbing to 3.8 per cent in April driven by fuel and food costs — add another dimension to the government’s calculations. Higher gold prices could feed into household inflation expectations, while the duty revenue from remaining imports provides fiscal headroom.

Economists were largely supportive of the move. “This is a necessary and overdue step,” said DK Joshi, Chief Economist at CRISIL. “When the country is facing a once-in-a-generation energy shock and forex reserves are under pressure, it makes sense to discourage discretionary imports. Gold is a store of value but it does not contribute to productive economic activity the way crude oil or industrial raw materials do.”

However, opposition parties criticised the move as evidence of the government’s failure to manage the economy effectively. Congress spokesperson Jairam Ramesh said the duty hike was “an admission that the government has lost control of the macroeconomic situation” and called it a “punishment tax on Indian families who traditionally invest in gold for weddings and financial security.” The party demanded a white paper on the government’s strategy for managing the economic fallout of the global energy crisis.

For consumers, the immediate impact is clear: gold jewellery and gold investments have become significantly more expensive overnight. Jewellers expect a sharp decline in footfall and purchases in the near term, with the upcoming wedding season — traditionally the peak period for gold demand — likely to see muted buying. The government, for its part, will be watching closely whether the duty increase achieves its intended goal of reducing gold import volumes without triggering a parallel boom in smuggling and informal trade.