India’s Unicorn Club Reaches 87: How Fresh Funding Rounds Signal Renewed Confidence in the Startup Ecosystem

India’s unicorn count has climbed to 87 companies in early 2026, reinforcing the country’s position as the world’s third-largest startup ecosystem after the United States and China. But beyond the headline number, the more compelling story lies in how the composition, geographic distribution, and sectoral focus of India’s billion-dollar startups are evolving—reflecting a maturing ecosystem that is increasingly diverse, capital-efficient, and globally competitive.

The Current Unicorn Landscape: From Reliance Retail to Niche Innovators

India’s unicorn roster spans an extraordinary range of industries and business models. At the top, Reliance Retail commands a staggering $101 billion valuation, while Reliance Jio has secured $28.4 billion in cumulative funding—figures that reflect the scale of India’s consumer market. BYJU’S, despite its well-documented governance challenges, retains a $22 billion paper valuation, though its real market value remains a subject of intense debate.

Beyond these mega-valuations, the more instructive unicorns are those that have achieved billion-dollar status through capital-efficient growth in defined market segments. Companies such as Zerodha (online broking), Razorpay (payment infrastructure), Postman (API development platform), and Groww (investment platform) have demonstrated that Indian startups can build globally competitive products from Indian bases while maintaining financial discipline.

The 2026 crop of new unicorns shows a distinct shift toward enterprise technology and infrastructure plays, moving away from the consumer internet models that dominated the 2015-2021 vintage. Companies in B2B commerce, logistics technology, and vertical SaaS are increasingly reaching unicorn status, reflecting the formalisation and digitalisation of India’s business landscape.

The Path to Unicorn Status Has Changed

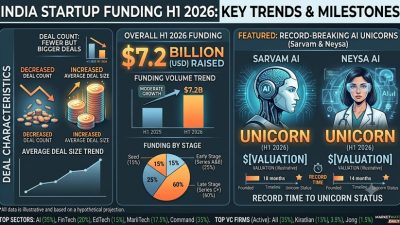

The journey to a billion-dollar valuation in India has evolved significantly from the growth-at-all-costs era. Today’s unicorn candidates typically demonstrate several characteristics that distinguish them from their predecessors: revenue run rates exceeding $100 million, improving or positive unit economics, diversified revenue streams that reduce concentration risk, and defensible competitive positions built on technology, data, or network effects rather than pure capital subsidisation.

This evolution is evident in the funding patterns. While earlier unicorns often achieved their valuations through large, quick successive rounds at rapidly escalating multiples, recent billion-dollar valuations have come after longer periods of operation and multiple rounds focused on milestone-based growth. The average time to unicorn status has increased from approximately 5 years in the 2020-21 cohort to 7-8 years for the current crop—a timeline more consistent with building genuine, sustainable businesses.

Sectoral Breakdown: Where India’s Unicorns Are Concentrated

Fintech remains the single largest category among Indian unicorns, with companies spanning payments (Razorpay, Pine Labs), lending (Lendingkart, Rupeek), insurance (PolicyBazaar, Digit Insurance), and investment platforms (Groww, Zerodha). The sector’s dominance reflects India’s massive unmet financial services demand and the enabling role of digital infrastructure—particularly UPI and Aadhaar—in creating addressable markets for fintech innovation.

E-commerce and consumer internet companies form the second-largest cluster, including horizontal marketplaces, vertical commerce platforms, and the quick commerce pioneers that are reshaping urban retail. The logistics and supply chain sector has also produced multiple unicorns, as companies like Delhivery, Xpressbees, and Ecom Express build the physical infrastructure that supports India’s digital commerce growth.

SaaS companies represent the most globally competitive segment of India’s unicorn landscape. Freshworks, Zoho (though technically bootstrapped and never formally a “startup”), Postman, BrowserStack, and Chargebee have built products with global customer bases, demonstrating that Indian startups can compete and win in international markets. The success of these companies has inspired a new generation of SaaS founders, as explored in discussions about India’s technology sector ambitions and structural development.

Geographic Diversification: Beyond Bengaluru and Delhi

While Bengaluru continues to be India’s startup capital, accounting for approximately 35 per cent of all unicorns, the geographic distribution is gradually broadening. Mumbai has strengthened its position as a fintech and consumer brand hub, while Delhi-NCR remains dominant in e-commerce, edtech, and D2C brands.

More notably, cities such as Pune, Hyderabad, Chennai, and Jaipur are producing an increasing number of high-growth startups. Pune’s deep-tech and enterprise software ecosystem has generated several companies approaching unicorn status, while Hyderabad’s healthcare and biotech startup cluster is gaining recognition. The government’s Startup India initiative and the proliferation of state-level startup policies have supported this geographic diversification.

The Unicorn Graveyard: Lessons From Failures

Not all unicorns have sustained their valuations or business models. The Indian startup ecosystem has witnessed several high-profile challenges: BYJU’S governance crisis, the difficulties faced by some quick commerce players, and valuation markdowns by public market investors in companies that listed at premium valuations have provided sobering lessons.

These experiences have shaped a more mature investor community that conducts deeper due diligence, insists on stronger governance frameworks, and pays closer attention to unit economics. The lessons have also influenced founders, many of whom now prioritise sustainable growth, responsible capital management, and building businesses that can withstand market cycles.

The Exit Environment: IPOs and Strategic Acquisitions

A critical factor in the unicorn ecosystem’s health is the exit environment. India’s IPO market has provided successful exits for several unicorns, with companies like Zomato, Nykaa, PolicyBazaar, and Delhivery having completed public listings. However, the mixed post-listing performance of some of these companies has introduced greater scrutiny into the IPO pricing and timing decisions for future unicorn listings.

Strategic acquisitions by larger companies—both Indian corporates and global technology firms—are becoming an increasingly important exit channel. Reliance, Tata, and other conglomerates have made multiple startup acquisitions, while global companies such as Walmart (Flipkart) and Google continue to view India as a strategic market for acquisition-led growth. The growing M&A activity aligns with the broader corporate consolidation trend detailed in our analysis of India’s $26 billion M&A surge and corporate dealmaking outlook.

Looking Ahead: India’s Path to 100 Unicorns

Industry projections suggest India could reach the 100-unicorn milestone by early 2027, supported by several tailwinds. The deepening of digital infrastructure, expanding internet penetration (now exceeding 800 million users), growing per capita income, and the government’s supportive policy environment all create favourable conditions for startup scale-up.

However, the quality of unicorns matters more than the quantity. The ecosystem’s long-term success will be measured not by how many companies cross the $1 billion valuation mark, but by how many build enduring businesses that create value for all stakeholders—customers, employees, investors, and the broader economy. As India’s startup ecosystem matures, the evolving financial landscape including the UPI revolution in digital payments provides the infrastructure on which the next generation of innovative companies will be built.

India’s 87 unicorns represent not an end point but a milestone in a much longer journey—one that is transforming the country from a labour cost arbitrage destination to a genuine hub of innovation, entrepreneurship, and value creation on the global stage.