Indian Markets Consolidate Near 24,000 — Nifty Opens Flat After Iran Deal Rally, HCL Tech Jumps 3%

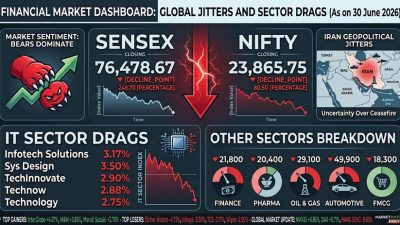

Indian stock markets opened Tuesday’s session on a cautious note as the Nifty 50 traded near 23,900 and the BSE Sensex hovered around 76,480, consolidating after Monday’s sharp Iran-deal-fuelled rally that added over ₹8 lakh crore to market capitalisation. The modest gains — Nifty up 51 points and Sensex up 216 points at the open — reflect a market that is digesting the previous session’s euphoria while awaiting clarity on several fronts, including the US-Iran framework’s details, the upcoming Federal Reserve meeting, and the monsoon’s impact on inflation.

The day’s standout performer was HCL Technologies, which surged as much as 3 percent to touch ₹1,150 on the BSE after the company announced a $150 million strategic investment in Sarvam AI, India’s newest artificial intelligence unicorn. The investment, which gives HCLTech approximately 10.5 percent of Sarvam, was viewed positively by the market as a forward-looking strategic bet on India’s sovereign AI ecosystem.

Why Markets Are Consolidating

Monday’s rally was driven primarily by the US-Iran peace framework announcement and the resulting crash in crude oil prices. Brent crude fell over 4 percent toward $83 per barrel, providing significant relief to India’s import-dependent economy. However, the White House’s subsequent clarification that the framework is not a final peace deal — and that nuclear negotiations will take months — has introduced uncertainty that is tempering the initial euphoria.

Related: Sensex Drops Over 150 Points as US Renews Strikes on Iran — Brent Crude Rises and FIIs Pull Back

Technical analysts note that the Nifty’s approach toward the 24,000 resistance level on Monday — where it touched an intraday high of 24,011 — triggered profit-booking that pushed the index back toward 23,850 by the close. The formation of a flag pattern near resistance suggests that the market needs a clear catalyst to break above 24,000-24,200 decisively. A failure to do so could result in range-bound trading between 23,600 and 24,000 in the near term.

“The sharp correction in Brent crude to below $84 and stability in the rupee have the potential to impart resilience to the market,” noted a market strategist. “The strong macro headwind of rising balance of payments deficit is no longer a serious issue. This positive development has imparted stability to the rupee, which has appreciated to 94.71 against the dollar from the recent low of 96.96.”

Sector-Wise Action

IT Sector: Technology stocks were in focus following the HCLTech-Sarvam AI deal. HCLTech’s gains lifted the broader IT index, with Infosys, TCS, and Wipro also trading in the green. The sector benefits from the weaker US dollar and improved global risk appetite, though concerns about AI’s impact on traditional IT services revenues continue to linger.

Banking: The Nifty Bank index traded marginally higher, supported by expectations that lower oil prices could give the Reserve Bank of India more room for rate cuts. HDFC Bank, ICICI Bank, and State Bank of India were among the top index contributors, with the sector benefiting from the improved macroeconomic outlook.

Oil Marketing Companies: OMCs continued to attract buying interest, with Indian Oil Corporation, BPCL, and HPCL extending Monday’s gains on expectations that sustained lower crude prices would improve their marketing margins and reduce inventory losses.

FMCG and Consumer: Consumer stocks showed mixed performance, with the monsoon forecast creating uncertainty. A weak monsoon could impact rural demand — a key driver for FMCG companies — while potentially pushing up food prices and squeezing consumer spending power.

Key Macro Factors to Watch

Several macroeconomic factors are shaping market sentiment this week:

1. US Federal Reserve Meeting: The Fed’s upcoming policy decision will be closely watched for signals on interest rates and inflation. If sustained lower oil prices alter the Fed’s inflation calculus, it could accelerate the timeline for rate cuts — a development that would be positive for emerging market assets, including Indian equities.

2. Crude Oil Trajectory: Brent crude’s decline toward $83 has been the single most important catalyst for the recent rally. If the Geneva signing proceeds smoothly on June 19 and Hormuz shipping normalises, oil could test the $70-75 range — providing further fuel for Indian markets. However, any escalation in Israel-Lebanon fighting could reverse the decline.

3. Monsoon Progress: The IMD’s below-normal monsoon forecast has introduced a new concern for markets. A weak monsoon could push inflation higher through food price pressures, constraining the RBI’s ability to cut rates and potentially impacting rural consumption — both negatives for equity markets.

4. India Wholesale Inflation: May wholesale price inflation came in at 9.68 percent, highlighting persistent supply-side price pressures. The market will be watching for signs of whether the crude oil decline translates into softer inflation readings in the coming months.

For investors, the near-term outlook calls for disciplined positioning. The macro tailwinds from lower oil prices and the Iran deal are real, but the combination of elevated valuations, monsoon uncertainty, and unresolved geopolitical risks suggests that selective stock-picking — rather than aggressive directional bets — is the appropriate strategy.

Also Read

- Sensex Jumps Nearly 1,000 Points and Nifty Surges Past 24,200 as Election Trends and Easing Iran Tensions Fuel Massive Stock Market Rally

- Sensex Surges 1100 Points, Nifty Reclaims 24000 as Crude Oil Crashes on Iran Peace Deal

- Sensex Rallies Over 900 Points and Crosses 76,300 as Crude Oil Prices Plunge 5 Percent — Nifty50 Nears 24,000 Mark

- Sensex Surges Over 500 Points and Nifty Crosses 23800 as Middle East Peace Hopes and Nvidia Earnings Drive Global Market Rally

- Sensex Crashes Over 840 Points, Nifty Slips Below 23,100 as Global Sell-Off Triggered by AI Bubble Fears and Surging Oil Prices Hits Dalal Street